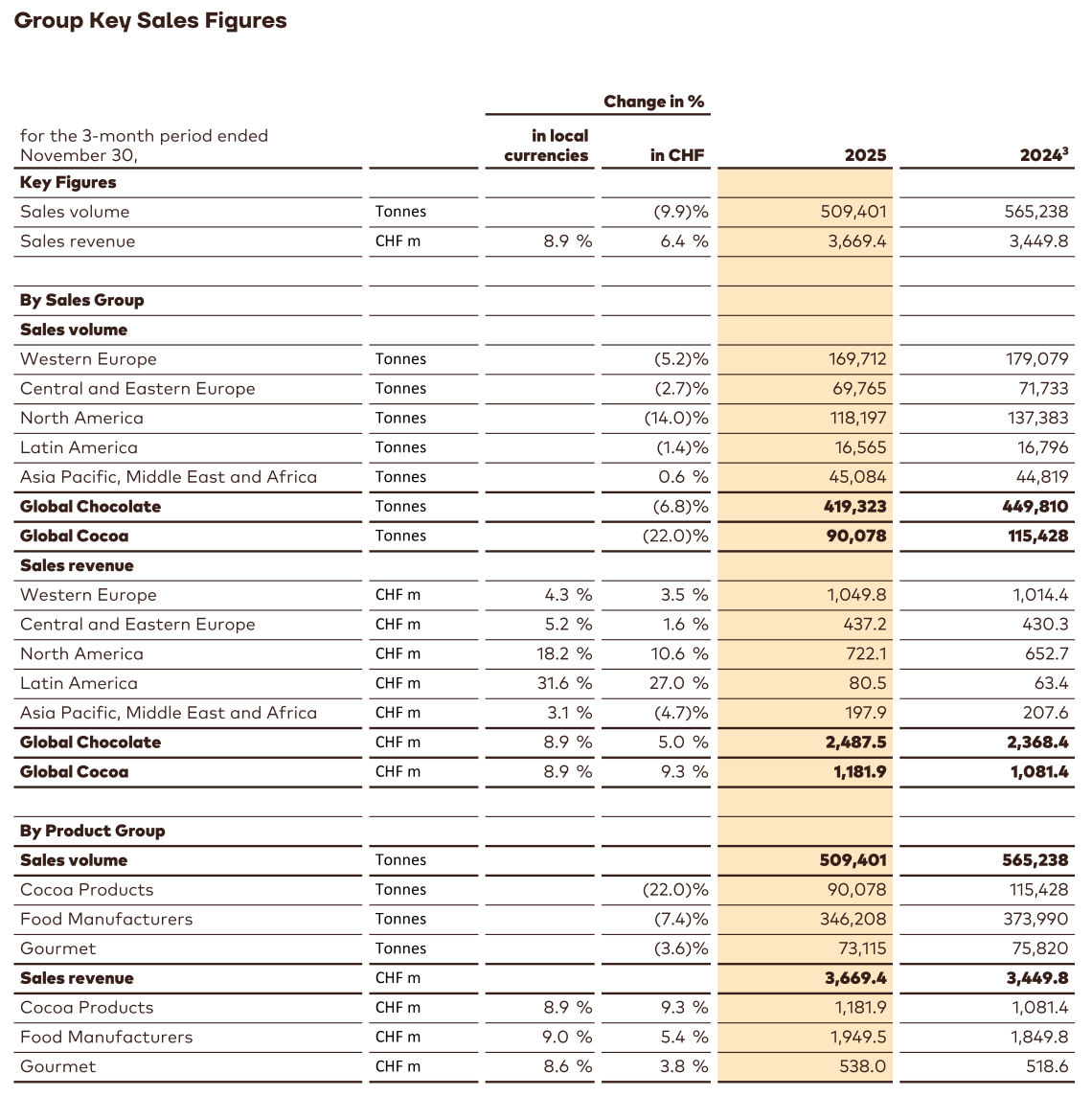

Barry Callebaut Group - 3-Month Key Sales Figures Fiscal Year 2025/26

Ad hoc announcement pursuant to Art. 53 LR

Barry Callebaut Group - 3-Month Key Sales Figures Fiscal Year 2025/26

Ad hoc announcement pursuant to Art. 53 LR

Anticipated soft start to the year, with lower cocoa bean prices encouraging sign for market stabilization.

As anticipated, the first quarter of our fiscal year began softly. Volumes in the global chocolate confectionery market deteriorated sequentially, as customers adjusted their behaviors and consumers temporarily reacted to higher prices. This challenging environment, together with the temporary production pause at our St. Hyacinthe facility due to a technical malfunction which has now been resolved, impacted our Global Chocolate performance. Our strategic decision to prioritize higher return segments and geographies in Global Cocoa also weighed on volume. Encouragingly, cocoa bean prices have reduced further since the start of the year and the crop is developing in line with our expectations. This is a positive signal for customer confidence and market behavior into the second half of the year. Looking ahead, our clear priorities for FY 2025/26 are to prepare for a return to growth and to further deleverage. We remain fully committed to our integrated cocoa and chocolate strategy which creates significant competitive advantage and value for all stakeholders.

1 Source: Nielsen volume growth excluding e-commerce – 26 countries, September 2025 - October/November 2025. Data subject to adjustment to match Barry Callebaut's reporting period. Nielsen data only partially reflects the out-of-home and impulse consumption.

Downloads

Media Assets

-

Barry Callebaut Chief Financial Officer, Peter Vanneste

Barry Callebaut Chief Financial Officer, Peter Vanneste -

Barry Callebaut Group 3-Month Key Sales Figures Fiscal Year 2025/26

Barry Callebaut Group 3-Month Key Sales Figures Fiscal Year 2025/26

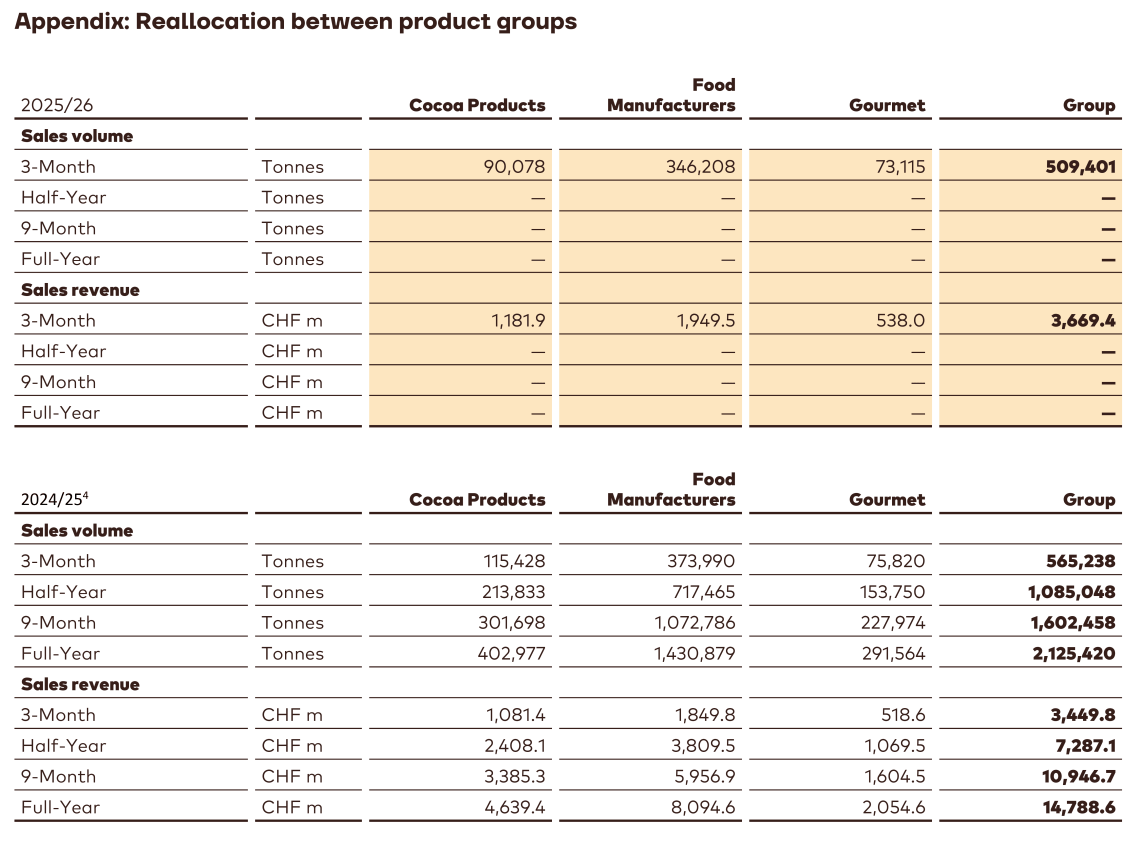

3 Certain customers have been shifted to a different product group to better serve them. The minor reallocation represented less than 1% of the total volume and sales revenue in fiscal year 2024/25.

4 Certain customers have been shifted to a different product group to better serve them. The minor reallocation represented less than 1% of the total volume and sales revenue in fiscal year 2024/25.

Follow the Barry Callebaut Group: