9-Month Key Sales Figures Fiscal Year 2024/25 of the Barry Callebaut Group

Ad hoc announcement pursuant to Art. 53 LR

9-Month Key Sales Figures Fiscal Year 2024/25 of the Barry Callebaut Group

Ad hoc announcement pursuant to Art. 53 LR

Chocolate volume impacted by exceptional cost-plus pricing, with strategic prioritization resulting in lower Cocoa volume

Over the past 18 months our industry has faced unprecedented disruption and volatility. Consistent with our commercial model, we have priced through the cocoa price increases to our customers. Meanwhile, customers are managing end-consumer price increases, causing short-term B2B disruption, further impacting our volume. The third quarter was impacted by our prioritization of volumes in the Global Cocoa business. We are working closely with our customers to develop more cost-effective solutions, leveraging the comprehensive strength of our full chocolate solutions portfolio. At the same time, our BC Next Level investment program is enhancing our agility and resilience to cocoa bean price volatility, with an emphasis on optimizing returns and reducing leverage.

1 On a recurring basis in local currencies.

2 Source: Nielsen volume growth excluding e-commerce – 26 countries, September 2024 - April/May 2025. Data subject to adjustment to match Barry Callebaut's reporting period. Nielsen data only partially reflects the out-of-home and impulse consumption.

Downloads

Media Assets

-

Barry Callebaut CEO, Peter Feld

Barry Callebaut CEO, Peter Feld -

Barry Callebaut Chief Financial Officer, Peter Vanneste

Barry Callebaut Chief Financial Officer, Peter Vanneste -

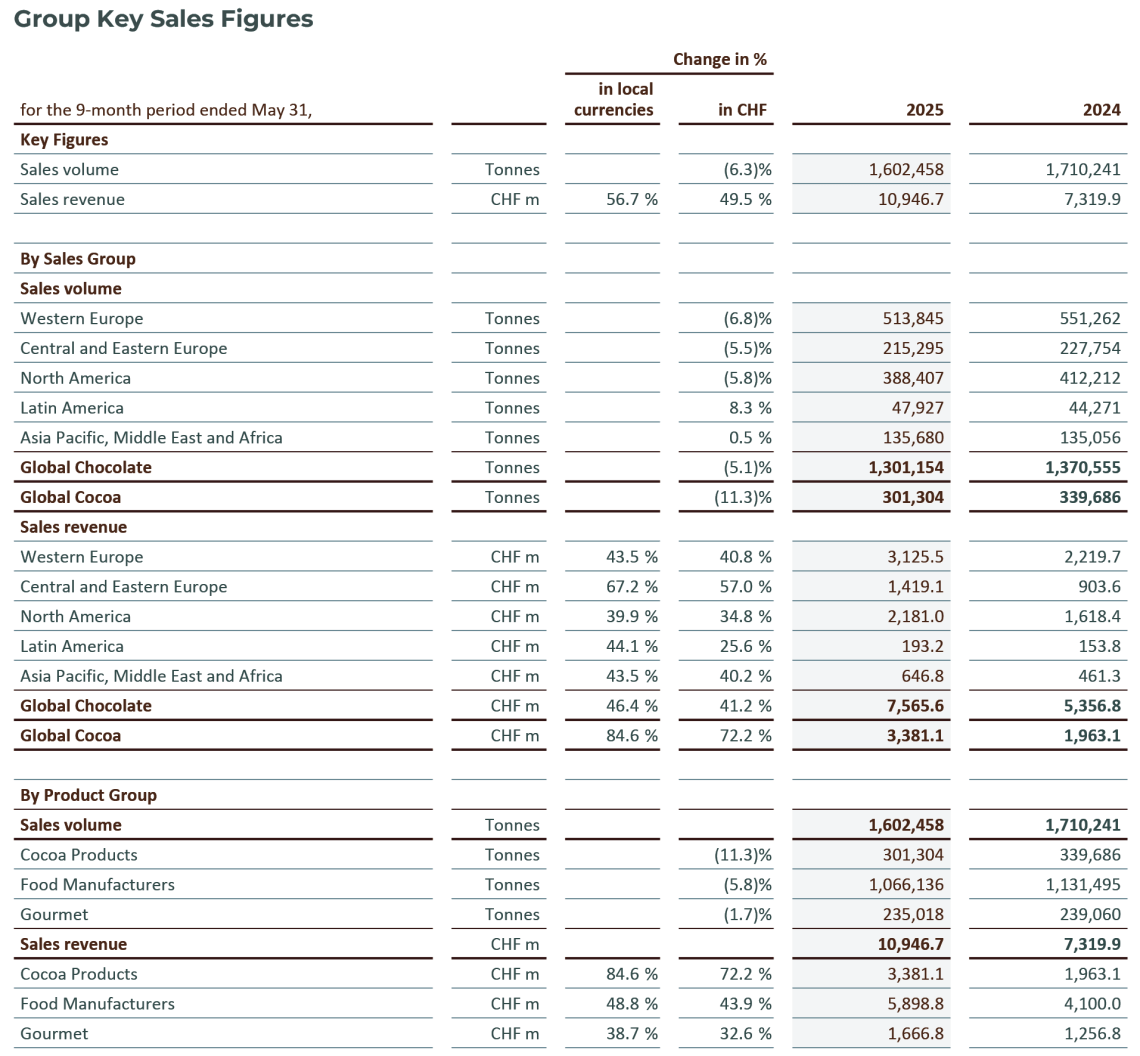

Barry Callebaut 9-Month Key Sales Figures, Fiscal Year 2024-25

Barry Callebaut 9-Month Key Sales Figures, Fiscal Year 2024-25

Follow the Barry Callebaut Group: