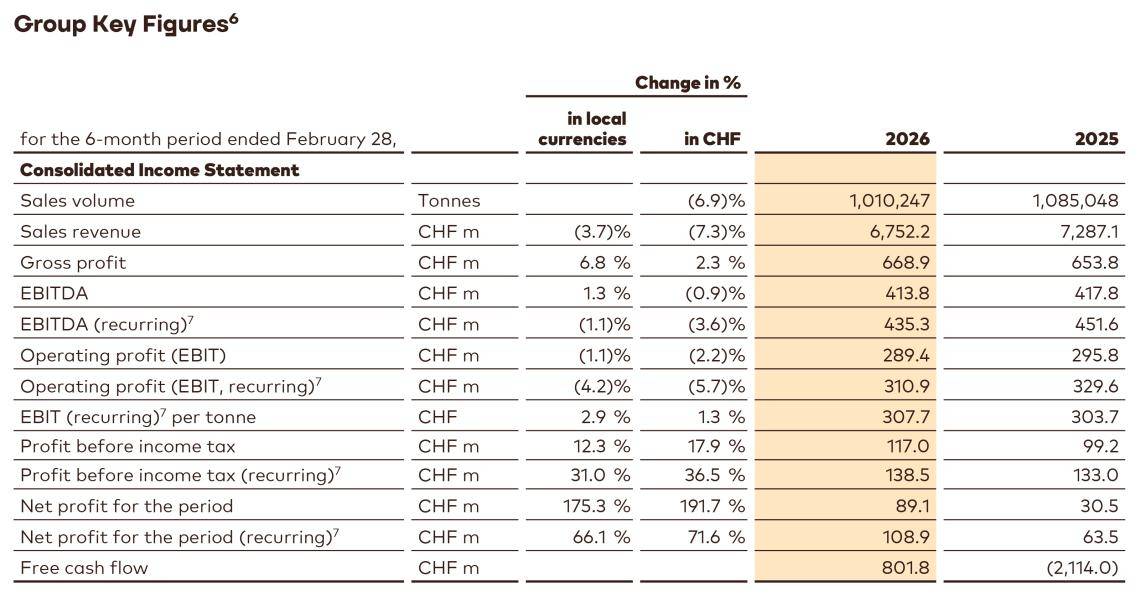

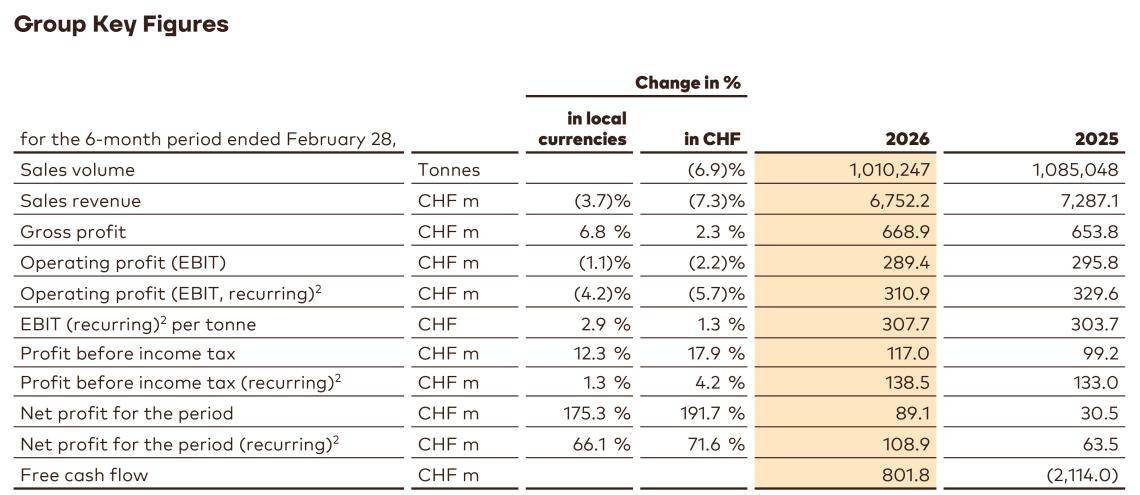

Barry Callebaut Group sales volume decreased by -6.9% to 1,010,247 tonnes in the first six months of fiscal year 2025/26 (ended February 28, 2026). In the second quarter, volume remained impacted by negative market dynamics while improving sequentially to -3.6%, driven by a return to growth in AMEA and Latin America.

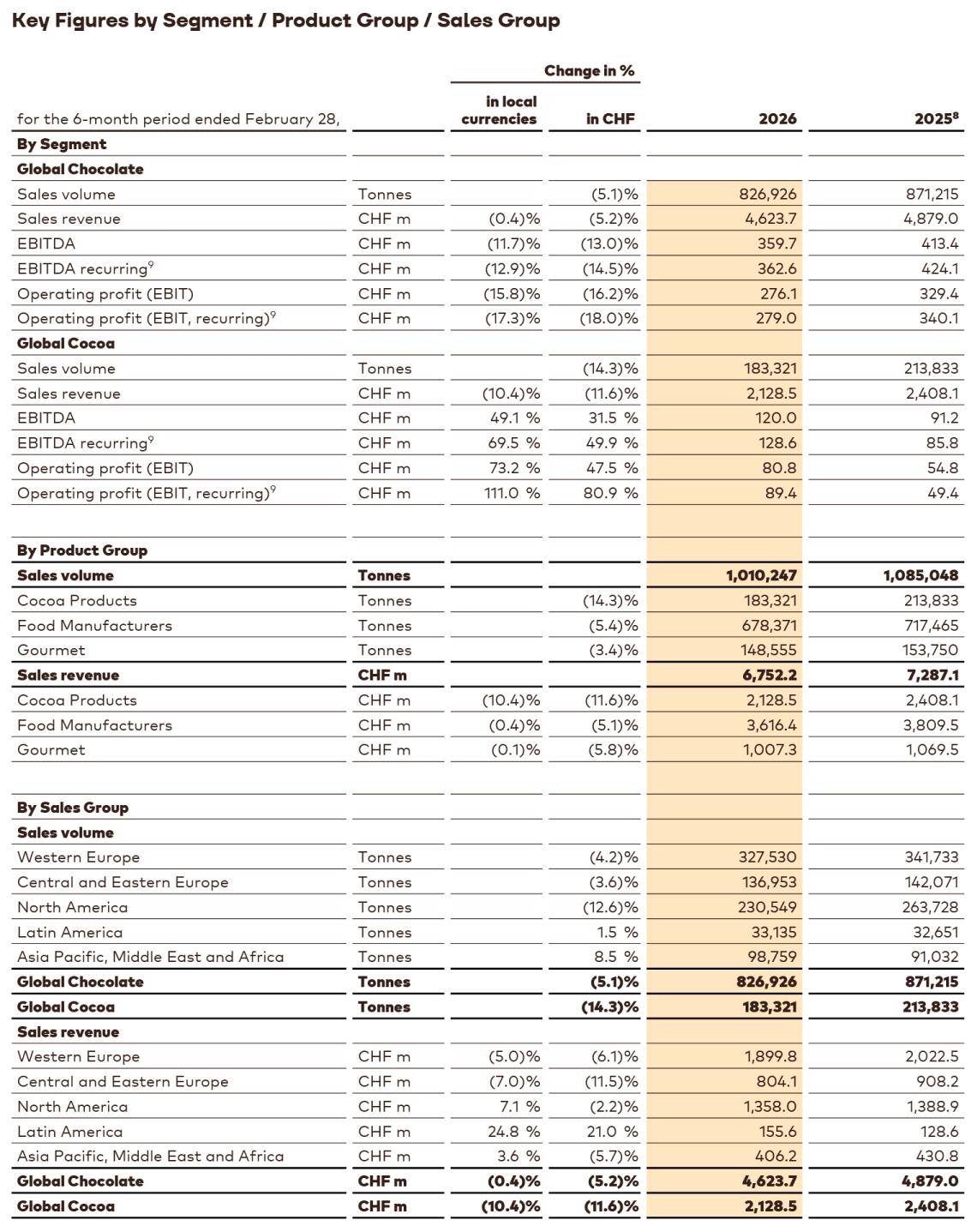

Global Chocolate volumes decreased by -5.1%, ahead of the declining global chocolate confectionery market according to Nielsen3 (-6.5%). Volume development in Food Manufacturers (-5.4%) was impacted by negative market dynamics as customers adapted behaviors in the context of lower demand, as well as by supply disruption in North America. Volumes in Gourmet decreased by -3.4% as competitiveness was temporarily pressured by a high price list in a declining cocoa price environment as well as by supply disruption.

Looking at regional performance within Global Chocolate, Asia Pacific, Middle East and Africa (AMEA, +8.5%) was the strongest contributor. Volume growth in AMEA reached double-digits in the second quarter driven by market share gains in China, momentum with key customers in India and additional business secured in Australia, partly offset by market pressure in Japan and South Korea. Latin America saw slightly positive volume growth (+1.5%) with solid growth in the second quarter, supported by strong performance in Gourmet. Central and Eastern Europe (-3.6%) was impacted by lower volumes for large Food Manufacturer customers due to challenging macroeconomic conditions, while local accounts saw solid growth especially in Türkiye. Volume development in Western Europe (-4.2%) was impacted by market demand softness. North America reported a volume decrease of -12.6%, reflecting network supply disruption following the temporary closure of the St. Hyacinthe factory in Canada in the first quarter and challenging market dynamics. North America saw sequential monthly improvement as the business rebuilds inventories and meets growing customer contracts and orders.

Sales volume for Global Cocoa declined by -14.3% as a result of negative market demand, particularly in AMEA, as well as the prioritization of volume towards higher profitability segments. The business saw a sequential volume improvement in the second quarter to -5.2%, with early signs of market improvement.

Sales revenue amounted to CHF 6,752.2 million, a decrease of -3.7% in local currencies (-7.3% in CHF) as a result of lower volume. In the second quarter, year-on-year cocoa-related pricing turned negative as a result of the cost-plus pricing model Barry Callebaut uses for the majority of its business.

Gross profit amounted to CHF 668.9 million, up +6.8% in local currencies (+2.3% in CHF), supported by strong cocoa profitability in a more favorable margin environment.

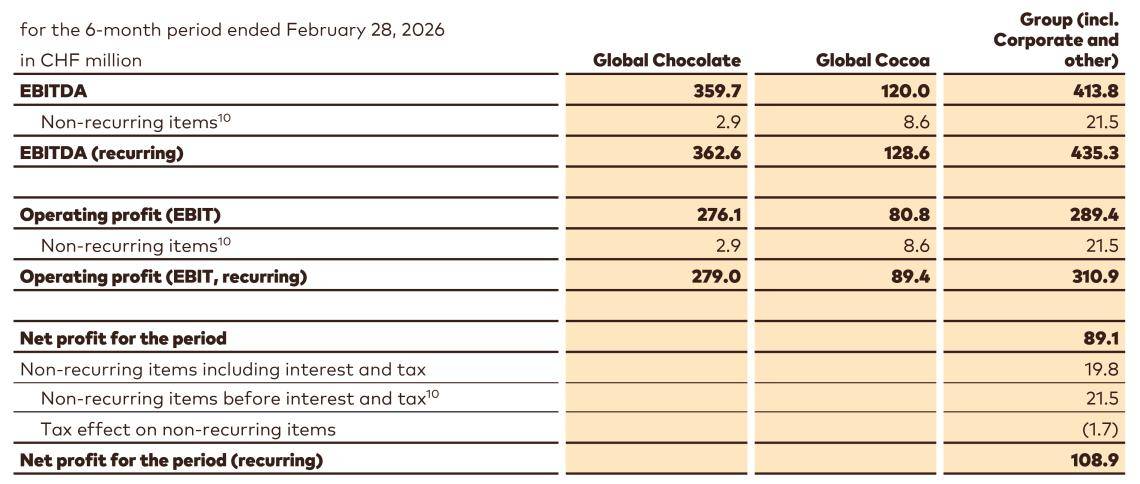

Operating profit (EBIT) recurring2 amounted to CHF 310.9 million, a decrease of -4.2% in local currencies (-5.7% in CHF) compared to the prior-year period. Cocoa profitability was strong, capturing a more favorable margin environment for cocoa. This was more than offset by the impact of volume decreases, supply disruption and a competitive overcapacity market. In particular, Gourmet margins were temporarily pressured by commercial investments related to its long position in a fast declining cocoa price environment. The decrease also reflects a reversal of financing cost pass-through, which negatively impacted EBIT but was neutral at a Net profit level.

Recurring4 EBIT per tonne amounted to CHF 308, up +2.9% in local currencies (+1.3% in CHF). Recurring4 EBIT for Global Chocolate was CHF 279.0 million, down -17.3% in local currencies (-18.0% in CHF) due to lower volumes, supply disruption and the intense competitive environment, particularly given a long Gourmet position in a fast declining cocoa market. Recurring4 EBIT for Global Cocoa was CHF 89.4 million, up +111.0% in local currencies (+80.9% in CHF), supported by a more favourable margin environment. EBIT reported was CHF 289.4 million, compared to CHF 295.8 million in the prior-year period (-1.1% in local currencies and -2.2% in CHF). Net one-off operating expenses amounted to CHF 21.5 million.

Profit before tax recurring4 amounted to CHF 138.5 million, an increase of +1.3% in local currencies (+4.2% in CHF). Net finance costs decreased to CHF -172.4 million compared to CHF -196.7 million in the prior-year period, mostly as a result of debt reduction with repayment of the EUR 263 million term loan in September 2025 and EUR 191 million Schuldscheindarlehen in February 2026 as well as reduction of commercial paper outstanding and bilateral facilities.

Net profit recurring4 amounted to CHF 108.9 million, up +66.1% in local currencies (+71.6% in CHF), supported by lower income tax expenses. On a recurring basis, income tax expense decreased to CHF 29.6 million versus CHF 69.4 million in the prior-year period. This corresponds to an effective tax rate of 21.4% (prior-year period: 52.2%), which mainly resulted from a more favorable mix of profit before taxes and much lower non-tax-effective losses in some countries. Net profit reported was CHF 89.1 million compared to CHF 30.5 million in the prior-year period.

Net working capital decreased to CHF 3,198.9 million from CHF 5,900.8 million in the prior-year period. The decrease was due to the positive impact from lower cocoa bean prices on inventory value and operational actions to reduce the working capital cycle and optimize sourcing.

Free cash flow generation amounted to CHF 801.8 million, compared to CHF -2,114.0 million in prior-year period, despite the peak harvest and cocoa buying season due to the significant cocoa bean price related working capital decrease and operational actions to reduce the cash cycle.

Net debt decreased significantly to CHF 3,604.3 million, compared to CHF 6,111.6 million in the prior-year period given the impact of lower cocoa bean prices and operational actions to reduce working capital. As a result, further significant deleverage progress was achieved with Net debt / EBITDA recurring declining to 3.9x compared to 6.5x in the prior-year period. When taking into consideration the cocoa bean inventories as readily marketable inventories (RMI), adjusted5 Net debt / EBITDA recurring was 2.7x.

3 Source: Nielsen volume growth excluding e-commerce – 26 countries, September 2025 - January 2026. Data subject to adjustment to match Barry Callebaut's reporting period. Nielsen data only partially reflects the out-of-home and impulse consumption.

4 Please refer to appendix on page 8 (in the PDF) for the detailed recurring results reconciliation.

5Net debt adjusted for cocoa bean inventories regarded by the Group as readily marketable inventories (February 2026: CHF 1,077.6 million; February 2025: CHF 3,192.5 million).

Barry Callebaut Chief Executive Office, Hein Schumacher

Barry Callebaut Chief Executive Office, Hein Schumacher Barry Callebaut Chief Financial Officer, Peter Vanneste

Barry Callebaut Chief Financial Officer, Peter Vanneste Barry Callebaut Half-Year Results Fiscal Year 2025/26

Barry Callebaut Half-Year Results Fiscal Year 2025/26